RECRUITMENT OF AN AUDITOR

AUDIT TERMS OF REFERENCE FOR AUDIT OF PLAN INTERNTIONAL BURKINA FASO du Project (CHAM” BFA100390 “Choisir avec Qui et Quand se Marier), GNO general donation, Germany Foundation and Austrian Foundation

Use and adapt these Terms of Reference to engage an audit firm when there are no donor-specified audit procedures.

1. Funds Background

Plan International Burkina Faso has been implementing the project Choisir avec qui et quand se Marier (CHAM)”, funded by the GNO general donation, Germany Foundation and Austrian Foundation with a total grant of EUR 1 787 000 for the period starting from 01st November 2019 to 30st November 2023 ; As stipulated under the project number BFA 100390. Plan International Burkina Faso wishes to engage the services of an audit firm for the purpose of auditing the project for the 1st grant period starting from 01st November 2019 to 30st November 2023 and the audit services will cover the Plan International Burkina Faso and subsequent partner organisation (sub-grantees) budget as indicated : Plan International Burkina Faso and Association d’Eveil Pugsada (ADEP) : Total Budget 1 787 000 EUR (1.172.195.159 XOF)

The auditor will carry out the audit of such statements of account in accordance with the following Terms of References.

The audit shall be reported in the following two documents in appendix 1 and 2, which includes an audit opinion in the submitted Auditor’s report and an attached Management letter describing the scope of the audit and factual findings.

2. Audit Objectives

The objective of the audit is to enable the auditor to express an independent professional opinion on :

2.1 Whether the financial position of the funded project, funds received and expenditures for the reporting period are presented fairly in all material respects in the financial report and in accordance with donor requirements ;

2.2 Whether the funds have been used in conformity with the provisions of the donor contract, including the approved budget and workplan and any amendments ;

2.3 Whether the financial report agrees with the financial accounts which provide the basis for

preparation of the financial report and reflect the financial transactions of the project ; and

2.4 Whether the financial report agrees or reconciles with other information reported to the donor such as narrative reports.

3. Responsibility for Preparing the Financial Report

The responsibility for the preparation of the consolidated financial report for each implementing organisation covered by the audit, if applicable, lies with Plan Inc.

4. Financial Statements

The financial statements should include the following components :

4.1. In the currency of the donor contract, an Income and Expenditure Statement showing funds received and all expenditures. Expenditures should be reported against the budget as defined in the donor contract for the period with the actual expenditure allocated to the same budget categories ;

4.2. A statement of financial position

4.3. A statement of changes in net assets

4.4. Any other footnotes applicable.

4.5. Supplemental statements on advances and fixed assets, including : (a) a statement or annex showing partner advances and reconciliation of total amount advanced by Plan to sub-grant partners with recorded expenditure and cash balances at the end of the reporting period, (b) a listing of all fixed assets purchased with grant funds.

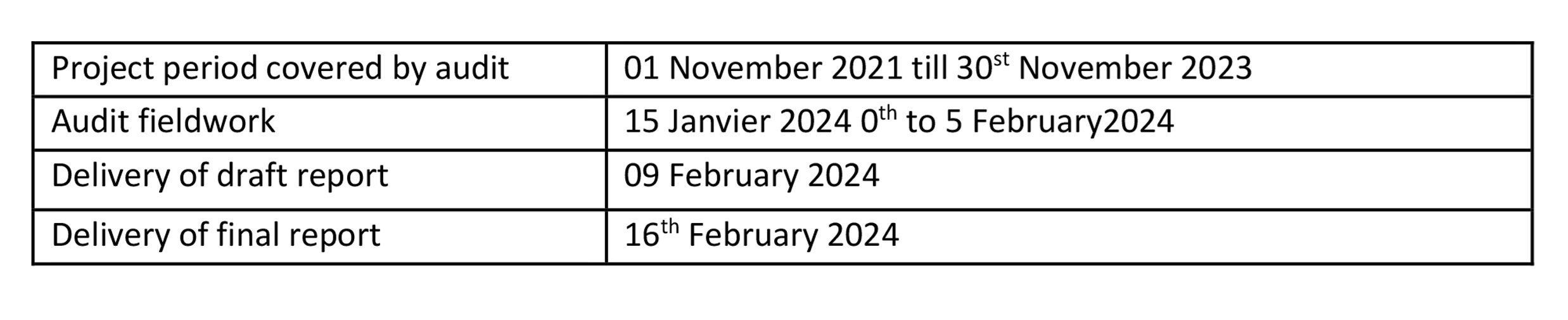

5. Timetable

The tasks that will be done by audit firm need to be completed, as timeline below :

6. Audit Scope of Work

6.1. The Audit shall confirm :

• The identity of the project concerned.

• In which way the audit has been carried out.

6.2. The audit should offer an opinion on the following areas :

• Does the Financial Project Report correspond with the agreement ?

• Are the recorded expenses in the Financial Project Report in line with the approved original budget and activity plan ?

• Is the approved Financial Project Report free of material misstatement ?

• Have the funds have been utilised in accordance with the approved budget and planned activities ?

• The organisation has kept registers of the Petty Cash and the Bank Accounts. In the absence of the project bank account, there are sufficient internal controls to monitor the project funds.

• Based on a representative selection, the expenditures are supported by original bills, duly cancelled, stamped and signed. Appropriate and approved internal procedures for authorising disbursements have been adhered to.

7. Auditor’s report

The audit shall be conducted in accordance with International Standards on Auditing (ISA) 800 “The Independent Auditor’s Report on Special Purpose Audit Engagements and as promulgated by the International Federation of Accountants and that standards used for the preparation of the financial statements are in accordance with the International Financial Reporting Standards.

The Auditor’s report shall include an audit opinion. See example and format for an Auditor’s report, appendix 1. The audit documents and report should be kept by the auditor for five years.

8. Management Letter

The auditor shall also, attached to the Auditor’s Report, submit a Management letter which needs to describe the purpose and the agreed-upon procedures of the engagement in sufficient detail to enable the reader to understand the nature and the extent of the work performed. The Management letter shall also include factual findings. See example and format for a Management letter attached to the Auditor’s report, appendix 2.

9. Reporting

Plan International Burkina Faso will forward the Auditor’s Report and Management Letter to the NO/Donor in [Country] through both email and regular mail or courier. The report should be in English.

10. Audit Report

The required number of copies of the signed report will be submitted by Plan international Burkina Faso both in hard copy and PDF soft copy.

Appendix 1 Example format for the Auditor’s Report

AUDITOR’S REPORT (IN ACCORDANCE WITH ISA 800/805) TO THE DONORS OF [CO Name] – [Project Name and grant #]

We have examined the financial statements for the Project “Choisir avec Qui et Quand se Marier” (CHAM) set out on pages.... The management is responsible for preparing the financial project report. Our responsibility is to report to you our opinion on the consistency of the financial report within the Project “Choisir avec Qui et Quand se Marier” (CHAM) and its compliance with agreement and regulations. We also read other information contained in the financial project report and consider the implications for our report if we become aware of any apparent misstatements or material inconsistencies with the summary financial statements whether due to fraud or error.

We conducted our audit in accordance with International Standards on Auditing (ISA 800/805), and the applicable parts of the agreement between GNO general donation, Germany Foundation and Austrian Foundation and Plan International Burkina Faso. Those standards require that we plan and perform the audit to obtain reasonable assurance that the financial statement within the financial project report is free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial report. An audit also includes assessing the accounting principles used and their application by the management and significant estimates made by the management when preparing the financial statement as well as evaluating the overall presentation of information in the financial statement. We believe that our audit provides a reasonable basis for our opinion set out below.

Basis of opinion

We conducted our work in accordance with ISA 800/805 “The Independent Auditor’s Report on Special Purpose Audit Engagements”.

Opinion

In our opinion, the financial report for the project is consistent with the accounting system, complies with the agreement and regulations and has been prepared in accordance with the agreement between GNO general donation, Germany Foundation and Austrian Foundation and Plan International Burkina Faso.

[Date and place]

[Name and title of auditor]

[Address]

Appendix 2 Example format for the Management Letter/Report of Factual Findings

REPORT OF FACTUAL FINDINGS

To [CO Name] Management

Scope of audit

We have performed the procedures agreed with you and enumerated below with respect to the financial project report as at [date] of [organisation]’s [Project name] , for the time period DD/MM/YYYY to DD/MM/YYYY showing total expenditure of [currency] [amount].

Our engagement was undertaken in accordance with [standards and regulations]. The procedures were performed solely to assist you your commitment to Plan International regarding the validity of the financial project report, and the following most important procedures were undertaken during the audit :

1. [Risk analysis according to ISA 315, describe the most significant standpoints in the planning of the audit]

2. [Review process of fraud and corruption according to ISA 240]

3. ……

4. ……

Outcome and significant observations

We report our findings below :

a) ….

b) ….

c)

Our report is solely for the purpose set forth above and for your information and is not to be used for any other purpose or to be distributed to any other parties than Plan International and [donor name].

[Date and place]

[Name and title of auditor]

[Address]

See guidance section 3.4